US Government Could Miss Payments as Soon as Dec. 21

WASHINGTON-A bipartisan think tank warned on Friday the U.S. government could start missing payments on its bills as soon as Dec. 21 if Congress fails to raise the debt limit, as top Democrats and Republicans sought a path around such a financial calamity.

The Bipartisan Policy Center’s projection, based on updated official data on tax receipts and government spending, underscores the mounting pressure on President Joe Biden’s Democratic Party to find a way to raise the statutory $28.9 trillion debt limit and avoid the heavy economic repercussions that could come with missed payments.

Earn up to $11 for every friend who reads this article.You can earn points by sharing articles to friends. With points, you can redeem for gift cards from 100+ top brands, or other benefits. Learn more

Congress passed legislation on Thursday to fund the government through mid-February, averting the risk of a partial government shutdown for now. But the task of bridging partisan differences over the debt limit could prove more difficult and pose risks that are far more severe.

“Congress would be flirting with financial disaster if it leaves for the holiday recess without addressing the debt limit,” said Shai Akabas, the Washington-based Bipartisan Policy Center’s director of economic policy.

If upcoming tax receipts are favorable, the center projected, the debt ceiling could become binding as late as Jan. 28.

On Tuesday, the nonpartisan Congressional Budget Office said the Treasury Department could start missing payments by the end of the month, while Treasury Secretary Janet Yellen said Washington can likely keep paying all its bills through at least Dec. 15.

Once the Treasury Department hits its borrowing limit, it will only have incoming tax receipts to pay its bills. And because it borrows nearly 40 cents for every dollar it spends, the Treasury would start missing payments owed to lenders, citizens, or both.

Shock waves would ripple through global financial markets. Domestic spending cuts would push the U.S. economy into recession as the government misses payments on everything from Social Security benefits for the elderly to soldiers’ salaries.

Biden’s Democrats hold razor-thin majorities in both houses of Congress, but Republicans have vowed not to cooperate on the debt ceiling, which could stymie attempts to lift borrowing limits under normal legislative rules.

In the Senate, Majority Leader Chuck Schumer (D-N.Y.) has demanded a “bipartisan” solution that would require Republicans to cooperate by allowing a debt ceiling measure to reach the floor. Republicans insist that Democrats use a more time-consuming legislative process known as “reconciliation” to raise the debt ceiling on their own.

Another sticking point is how to address the borrowing limit. Republicans want Democrats to raise the ceiling to a higher dollar amount, which they could then attack in 2022 congressional election ads. Democrats want to avoid a dollar amount by simply suspending the limit.

Watching, with disbelief and bemusement, how the “recovery-narrative” has been touted in the financial media and among some economists and analysts.

Categorically, an economic recovery is a period of expansion, where we eventually exceed the previous peak in employment and output. There’s no such thing coming (anytime soon).

It is very human to avoid acknowledging disturbing possibilities, such as the looming economic abyss the world economy is about to sink into, but now we absolutely need to perceive coldly the economic realities as they are. Otherwise, the effects of the approaching turmoil will be unbearable.

To help people and firms to think their way through the crisis, we summarize here the convincing counterarguments against this over-optimistic-and, in some cases even deceitful-recovery-narrative.

The diffusion index fallacy

Probably the biggest misunderstanding in the recovery-narrative is the misinterpretation concerning diffusion indexes like the purchasing managers indexes, or PMIs.

IHS Markit describes the PMI as:

“For each variable, the index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘no change’ responses. The PMI is a weighted average of the following five indices: New Orders (30%), Output (25%), Employment (20%), Suppliers’ Delivery Times (15%) and Stocks of Purchases (10%).”

All figures above 50 signal overall increase compared to previous month, while figures below 50 signal a decrease.

Now, during the lockdowns, PMIs crashed to range of 20 to 40, signalling a massive decrease in expectations and production. Now, the PMIs are mostly in a range from 50 to 60. What does all this imply?

The easiest way is to consider PMIs in terms of percentage changes. So, when index dives to 30, it signals a decrease of (roughly) 40 percent. How long does it take for the underlying series (production, sales, new orders, etc.) to recover to the level it was at before the decline?

All percent changes are relative. Let’s assume that there’s a decline of 40% in some monthly index from a level of 100 (to 60). With a monthly growth rate of 10 percent, it takes 6 months for the index to regain the 100 level. With a growth rate of five percent, it takes 11 months. With a growth rate of three percent, it takes 18 months. With a growth rate of two percent, it takes 26 months.

Stalling high-frequency data

Moreover, in the case of the PMIs (manufacturing and/or services) that are increasing, these are implying growth rates of 3 to 10 percent. So, even in the best-case we would be around six months away from an actual recovery, and serious doubts can be cast on the assumption that this growth rate can be sustained.

The so-called high-frequency indicators, which measure economic activity on a weekly basis, indicate that we have reached only around 60% to 80% of pre-Covid economic activity. Moreover, they have stabilized or even turned back down recently. This indicates that PMIs are likely to first stabilize around 50, and then turn back below 50 in the coming months.

If we look at the key economic indicators in the most important regions of the world, they also signal non-recovery in major economies.

The non-recovery of the US

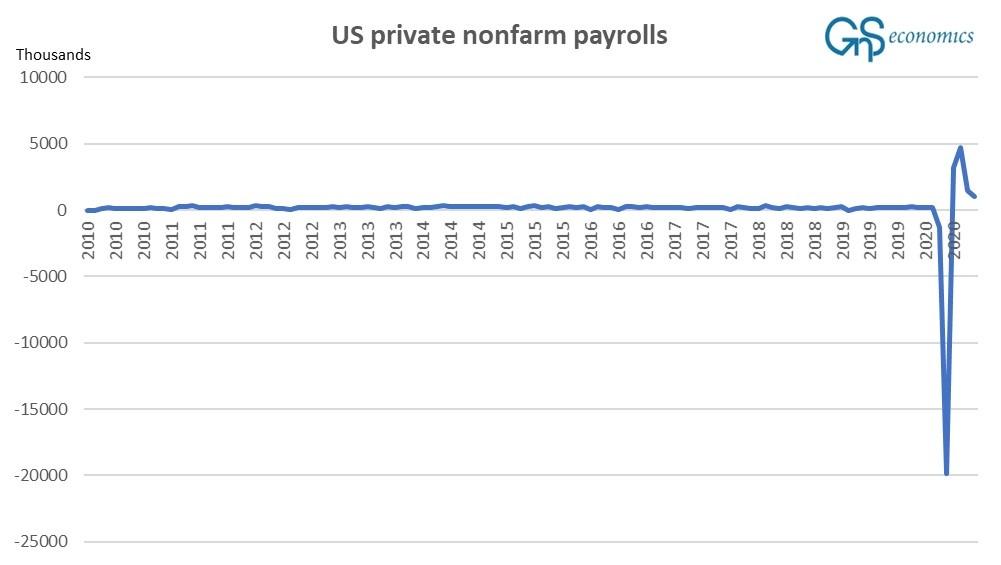

The consumer is the most important driver of the U.S. economy (private consumption accounts for close to 70% of U.S. GDP), and the biggest contributor to that is employment. Private employment crashed during the spring and it has since recovered only marginally. Its growth rate has stalled (see Figure 1).

While the pace of corporate bankruptcies have somewhat slowed, the large corporate bankruptcies still saw their biggest-ever increase in August. This makes any further notable improvements in employment unlikely.

The non-recovery of China and the Eurozone

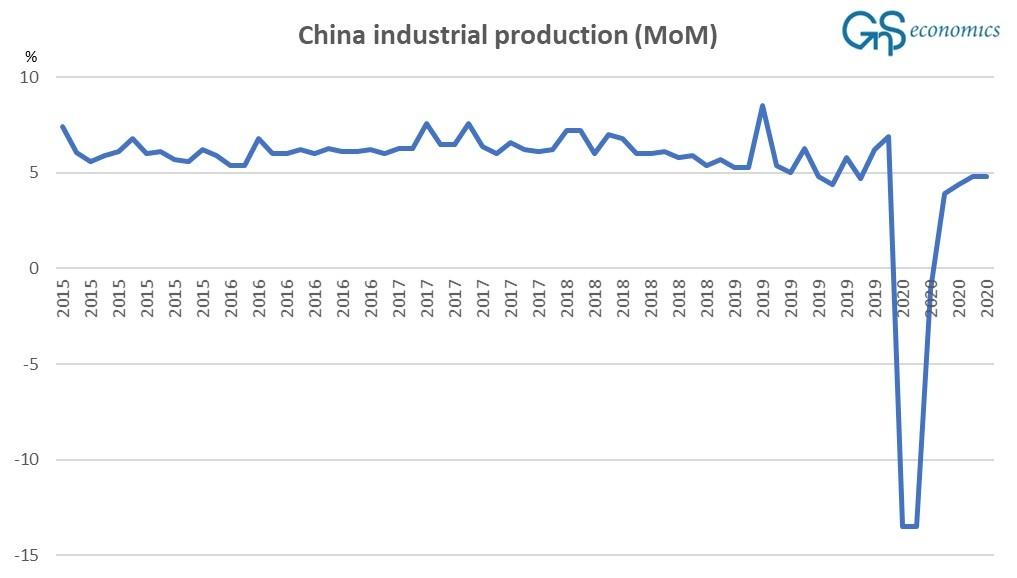

Industrial production is still the backbone of the Chinese economy, although the role of the consumer has grown.

Industrial production in China quite expectedly crashed in January and February of this year, and we have not observed any bounce powerful enough to return it to pre-Corona levels quickly (see Figure 2). With the current growth rate of 4-5%, it would take until around Christmas for the industrial production to reach the level where it was before the pandemic (in December 2019). And there are also serious doubts as to whether China can keep such a rapid growth pace up.

Retail sales have not recovered as expected, and in fact they actually declined (YoY) in July. Serious questions can also be entertained about a continuation of the Chinese recovery due to escalating problems in its over-levered banking sector.

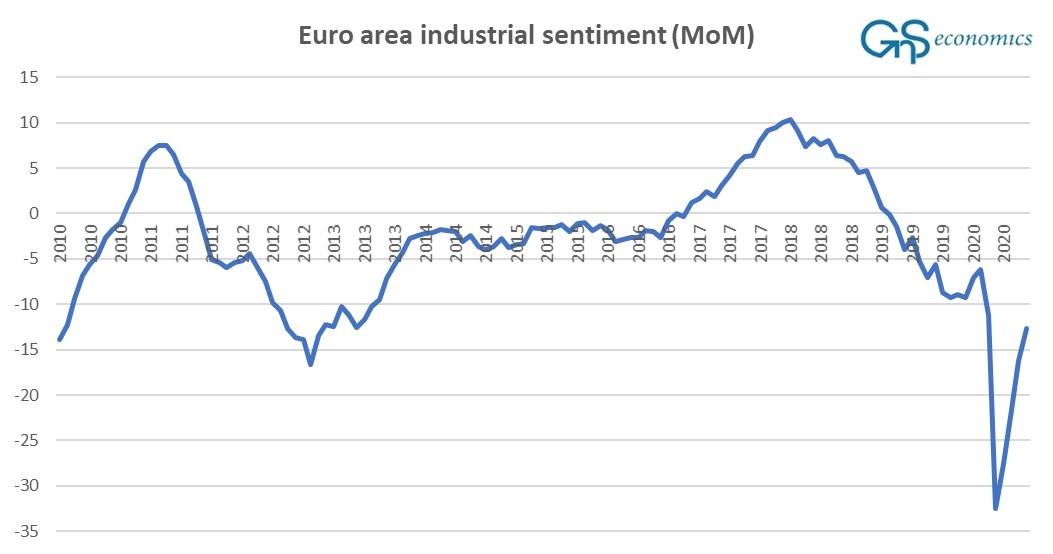

The Eurozone is the true ‘problem-child’ in the global recovery-narrative. It already succumbed to recession in Q4 2019 (see our recession warning from March). There are also very few signs of an actual recovery in the currency bloc, reflected, for example, in collapsed industrial sentiment, which has not recovered (see Figure 3). This does not bode well for the fragile European banking sector.

Failure of (yet more) stimulus

The third issue overlooked in the recovery-narrative is that whatever lacklustre recovery there is has only been achieved by truly colossal levels of fiscal and monetary stimulus.

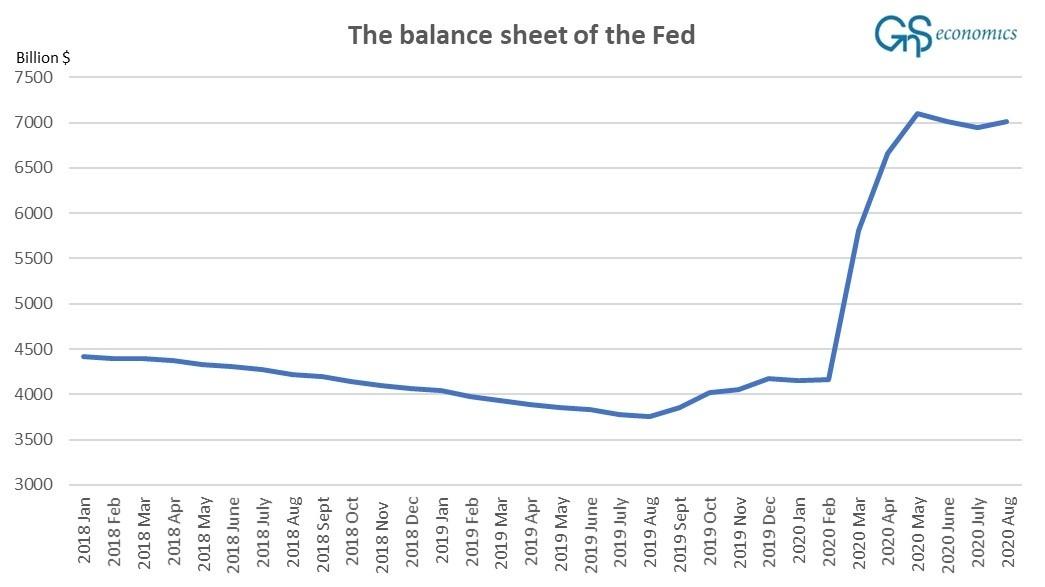

The U.S. government has flooded over $2 trillion into the economy and the budget deficit is expected to top $3.3 trillion in 2020, the largest deficit as a percentage of GDP since 1945. The balance sheet of the Federal Reserve has also exploded from little over $4 trillion to over $7 trillion in just a few months (see Figure 4). There is just one word for such unprecedented actions: desperation.

Stimulus in China has also broken records. By the end of July,’ the aggregate financing to the real economy’ had reached an astonishing $3.3 trillion, easily topping the previous record of $2 trillion set in 2019. In an economy that is already extremely indebted, this is, naturally, completely unsustainable.

There is, quite simply, no real economic recovery coming. On the contrary, we are heading deeper into the crisis.

We are bound to collapse

The lacklustre recovery from the massive economic impact of the coronavirus pandemic has been achieved with excessive fiscal and monetary stimulus in the most manipulated business cycle in modern history.

Moreover, the global business cycle was already very extended (record-breaking in the U.S.) and was in the process of rolling over. Central bankers and political leaders are effectively patching holes in a ship with whose decks are awash.

Business cycles are called cycles obviously because any economy proceeds through periods of both expansion and contraction. We have known this since Ancient Rome. Economic expansions always, always end.

However, the history of economic crises has also taught us that if a business cycle is artificially extended through monetary stimulation leading to excessive financial speculation, exactly as we are now experiencing, the risk of a catastrophic economic collapse is greatly increased. Alas, due to the ill-advised policies of central banks and political leaders, we are now bound to witness just such an event.

And it may turn out to be the worst economic crisis anyone has ever seen.

The World Is In Big Trouble, for Those That Believe We Will Go Back to Some Sense of Normal Life Here on Earth, You Will Be Sadly Disappointed, Seven and Half Years of Hell on Earth Which Began January 1, 2020

“Our courts oppose the righteous, and justice is nowhere to be found. Truth stumbles in the streets, and honesty has been outlawed” (Isa. 59:14, NLT)…We Turned Our Backs On GOD, Now We Have Been Left To Our Own Devices, Enjoy…

While Mainstream Media Continues to Push a False Narrative, Big Tech Has Keep the Truth From Coming out by Shadow Banning Conservatives, Christians, and Like-Minded People, Those Death Attributed to the Coronavirus Is a Result of Those Mentioned, They Truly Are Evil…

Source: theepochtimes HNewsWire zerohedge HNewsWire

StevieRay HansenEditor, HNewsWire.com

Watchmen does not confuse truth with consensus The Watchmen does not confuse God’s word with the word of those in power…

In police-state fashion, Big Tech took the list of accused (including this site), declared all those named guilty and promptly shadow-banned, de-platformed or de-monetized us all without coming clean about how they engineered the crushing of dissent, Now more than ever big Tech has exposed there hand engaging in devious underhanded tactics to make the sinister look saintly, one of Satan’s greatest weapons happens to be deceit…

The accumulating death toll from Covid-19 can be seen minute-by-minute on cable news channels. But there’s another death toll few seem to care much about: the number of poverty-related deaths being set in motion by deliberately plunging millions of Americans into poverty and despair.

American health care, as we call it today, and for all its high-tech miracles, has evolved into one of the most atrocious rackets the world has ever seen. By racket, I mean an enterprise organized explicitly to make money dishonestly.

All the official reassurances won’t be worth a bucket of warm spit. The Globals are behind the CoronaVirus, It Is a Man-Made Bioweapon.

![]()

Numerous times in our history since the founding of America, private banks have attempted to control and dominate this country.

“If the AmeThomas Jeffersonrican people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered.” – Thomas Jefferson

The most recent coup occurred in 1913 when President Woodrow Wilson signed into law the Federal Reserve Act, giving private banks the control of the issuance of our currency.

Much of the hostility toward private wealth comes from the hatred of its ability to insulate the citizen from the will of the state.