HNewsWire: America’s economic crisis is deepening “is “by design,” “everything was planned,” With two quarters of negative growth, we’ve already entered a technical recession.

Democrats are fomenting an economic calamity as a pretext for consolidating even more power and control in the hands of the government and its affiliated corporations.

“They’re just buying time because they know things are going to get much worse; it’s all planned because they need that moment of catastrophic economic collapse to drive through their socialist scheme.”

Political observers are warned not to dismiss political elites as oblivious to the consequences of their own abuses of power.

“I’m fed up with people giving them the benefit of the doubt. They said it was only temporary because they didn’t know what else to do. They were, of course, aware. Everything is done on purpose. Everything is going according to plan.

![]()

The collapse of the banking industry has started, with FDIC-insured Big Tech Silvergate Bank announcing yesterday they were liquidating their assets and closing down.

Silicon Valley Bank also announced yesterday that they have lost $10 billion, while trying to reassure depositors to just “stay calm,” suggesting that their collapse is also probably imminent.

I don’t think there has been a more significant news event in the financial sector since the financial crisis of 2008, and yet at the time of my publishing this article, none of the corporate media is treating this as a headline story, unless it is a publication that focuses only on financial news.

This is the beginning of the storm that should have happened last year after FTX blew up, and probably did, but the infection that I have been calling The Big Tech Crash that started in 2022 has only just now begun to reveal how serious this crisis is, which can no longer be hidden from the public as the bank failures have now begun.

Bank runs that began last year, are only going to significantly increase in the days and weeks ahead. And this infection is not confined to Big Tech and their banks, but is spreading fast to other sectors of the economy.

Silvergate Bank: Crypto Fraud Casualty

Image source.

Image source.

It certainly is not surprising that Silvergate Bank was the first to go, as they were the bank most heavily invested in cryptocurrencies. They are the first U.S. FDIC insured bank to collapse since the COVID crisis in 2020.

The holding company for the California-based Silvergate Bank announced on Wednesday that it would begin the process of ending its operations and voluntarily liquidating the bank, ending a long descent for the crypto-focused firm and weeks of speculation about its viability.

With crypto’s rise and traditional banks’ hesitance to work with the volatile sector, Silvergate had established itself as one of the most important partners for the nascent industry, offering key financial services in exchange for soaring profits. By working with crypto’s top companies, from Coinbase to FTX, Silvergate’s share price rose more than 1,500% between November 2019 and November 2021.

The bank’s fortunes were tied to the industry, with 90% of its deposit base coming from crypto companies. As the bear market set in, Silvergate suffered severe outflows, including $8.1 billion in digital asset deposits in the fourth quarter of 2022 alone, exacerbated by the November collapse of one of its key clients, FTX. (Full article.)

As Bloomberg reports, Silvergate collapsed amid scrutiny from regulators and a criminal investigation by the Justice Department’s fraud unit into dealings with fallen crypto giants FTX and Alameda Research. Though no wrongdoing was asserted, Silvergate’s woes deepened as the bank sold off assets at a loss and shut its flagship payments network, which it called “the heart” of its group of services for crypto clients. (Full article.)

The same day that Silvergate announced it was liquidating its assets and closing, Silicon Valley Bank made a surprise announcement that it would sell billions of dollars in stock to shore up its balance sheet and liquidate nearly all the securities it had available to sell so it could reinvest the proceeds.

The bank has suffered big losses on U.S. treasuries and mortgage-backed securities at the same time as its tech-heavy customers were burning through their deposits, according to The Information.

Things only got worse today (March 9, 2023), when Silicon Valley Bank CEO Greg Becker told top venture capitalists in Silicon Valley to “stay calm” amid concerns around a capital crunch that wiped nearly $10 billion off the bank’s market valuation.

I don’t know who wrote Becker’s script for this announcement, but having a bank CEO tell depositors and investors to “stay calm” is probably the WORST thing he could have said. It will probably have about the same effect as telling a crowded theater where a fire has just started to “just stay calm” and don’t leave the theater.

Silicon Valley Bank CEO Greg Becker on Thursday told top venture capitalists in Silicon Valley to “stay calm” amid concerns around a capital crunch that wiped nearly $10 billion off the bank’s market valuation.

On a call, Becker said that “calls started coming and started panic.” He added that the bank has “ample liquidity to support our clients with one exception: If everyone is telling each other SVB is in trouble, that would be a challenge.”

“I would ask everyone to stay calm and to support us just like we supported you during the challenging times,” he said. (Source.)

Too late Mr. Becker. The cat is out of the bag: Silicon Valley Bank IS in trouble.

And so is the rest of the financial system, as this Big Tech infection is not confined to just technology, as the U.S. society has spent decades now integrating technology into just about every other sector of our lives.

One of those sectors is the housing industry, as Better.com, a technology-based provider of mortgages, is also on life support, having laid off about 90% of their employees.

As The Information reported yesterday:

Better.com is staring into the abyss. The SoftBank-backed mortgage lender is fighting to survive amid high interest rates that have crushed its core refinancing business.

In an interview with The Information, its founder and CEO-who went viral in late 2021 when he sacked 900 employees on a Zoom call-didn’t rule out further staff cuts, even though previous layoffs have already shrunk Better.com’s headcount to 1,200 from 11,000 in 2021.

In the interview, Vishal Garg also described a multitude of rabbits he’s seeking to pull out of his hat.

Better.com faces deep challenges. In 2020 and early 2021, its business exploded thanks to low interest rates that drew a surge of mortgage refinancings. But refinancing interest has dried up as interest rates have soared. After posting a $172 million profit in 2020, Better lost $304 million in 2021 and another $328 million in the first quarter of 2022, according to securities filings by Aurora Acquisition Corp., a special purpose acquisition company that in 2021 proposed a merger with Better.com.

Other hurdles have arisen: Aurora disclosed last summer that the Securities and Exchange Commission was probing Better.com and the SPAC “to determine if violations of the federal securities laws have occurred.” (Read the full article at The Information – Subscription needed.)

Another sector heavily invested in technology is “healthcare.”

In a report published at Fierce Biotech yesterday, Johnson & Johnson announced that they were beginning layoffs in their “medtech division.”

![]()

The corporate media is now widely reporting on this, and the entire banking sector took a huge hit today, losing $billions in valuation, $52 billion lost just with the four largest banks in the U.S.

Bank runs and bank failures are no longer an “if,” but simply “when.” Which ones are next?

Banks Lose Billions in Value After Tech Lender SVB Stumbles

Investors dumped shares of SVB Financial Group SIVB -60.41% and a swath of U.S. banks after the tech-focused lender said it lost nearly $2 billion selling assets following a larger-than-expected decline in deposits.

The four biggest U.S. banks lost $52 billion in market value Thursday. The KBW Nasdaq Bank Index notched its biggest decline since the pandemic roiled the markets nearly three years ago. Shares of SVB, the parent of Silicon Valley Bank, fell more than 60% after it disclosed the loss and sought to raise $2.25 billion in fresh capital by selling new shares.

Banks big and small posted steep declines. PacWest Bancorp fell 25%, and First Republic Bank lost 17%. Charles Schwab Corp. fell 13%, while U.S. Bancorp lost 7%. America’s biggest bank, JPMorgan Chase & Co., fell 5.4%.

![]()

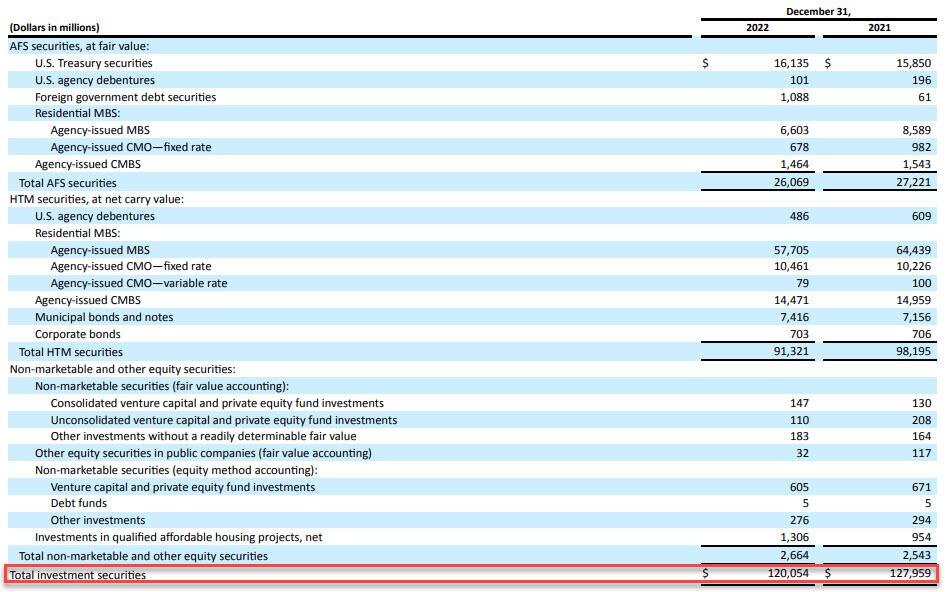

For those who slept through yesterday, here is what you missed and why the US banking system is suffering its worst crisis since 2020. Silicon Valley Bank, aka SIVB, the 18th largest bank in the US with $212 billion in assets of which $120 billion are securities (of which most or $57.7BN are Held to Maturity (HTM) Mortgage Backed Securities and another $10.5BN are CMO, while $26BN are Available for Sale, more on that later )…

… funded by over $173 billion in deposits (of which $151.5 billion are uninsured), has long been viewed as the bank at the heart of the US startup industry due to its singular focus on venture-capital firms. In many ways it echoes the issues we saw at Silvergate, which banked crypto firms almost exclusively.

SIVB stunned markets on Thursday after it announced a series of actions to improve its balance sheet flexibility and capital ratios as rates potentially remain higher-for-longer and private markets remain under pressure. Note: while many had speculated that the bank may be facing a liquidity crisis in a rapidly rising rate environment (most notably the WSJ in late 2022), it took the management team’s confirmation that liquidity has collapsed to spark a bank crisis and a depositor run. The bank said it sold $21 billion of its available for sale (AFS) securities to be reinvested into shorter-duration Treasuries, and publicly announced raising $2.25 bil of equity ($1.75 bil common and $0.5 bil pref) primarily to support its capital ratios given the $1.8 bil after-tax loss it expects to realize on the sale and also partly to help support its credit rating. We now know, courtesy of CNBC reporting, that this equity raise failed and the bank is instead is trying to sell itself to a bigger bank.

Why did SIVB do this? Well, according to Morgan Stanley’s Manan Gosalia, who as of yesterday was the only sellside analyst to have a Sell rating on the company with a $190 price target…

… the bank did not intend to spark a panic but instead “these actions enhance its balance sheet flexibility as rates move higher. By selling down its existing AFS portfolio, which had a duration of 3.6 years, and reinvesting the proceeds into short-term US Treasurys, SIVB is enhancing its liquidity position and NIM protection as rates continue to rise. The bank is also terming out its funding by adding $15 bil of longer-dated borrowings and hedging to protect against further increases in rates. All in, the bank estimates that it will flip to asset sensitive with each 25 bp increase in rates driving $50-60 mil of higher NII.“

In English? The bank had a lot of fixed-rate TSY (and other) exposure that was underwater and carrying an unrealized loss, and having concluded that rates will keep rising, the bank decided to restructure its assets and flip its portfolio from a fixed-rate one (where rate hikes cause even more capital losses) to a short-term one (where they lead to modest NIM gains). Of course, the transition ended up costing the bank billions.

None of this is shocking, and yet the market was clearly surprised. Why?

For the answer we have to go all the way back to the immediate aftermath of the last financial crisis, when in early 2009 US regulators suspended Mark to Market, and instead of having banks hold debt securities on their books at price, they allowed them to split their asset holdings into two components: Available for Sale (or AfS), a bucket which would be marked to market and which could be sold to short up liquidity, and Held to Maturity (or HTM), a (far larger bucket) which allowed the banks to keep debt securities at cost.

This was created to avoid cross-selling contagion if one bank was forced to liquidate securities and infect other holders of the same security. In other words, it was purely a idiosyncratic feature, not one that was meant to offset macro conditions. And understandably so: in a time of raging deflation, and ZIRP and QE, when rates would seemingly never go up, virtually nobody even considered a scenario when it would be the Fed itself that would force rates higher to fight galloping inflation.

Sadly for SIVB, that’s where we are now, and the Fed’s rate hikes have manifested in two ways.

- First, rising rates afford depositors a completely risk-free way of parking your money at Treasuries without taking on company-specific deposit risk. This is a big issue for SIVB because as noted above it has $170BN in deposits.

- Second, rising rates force the bank to sweep ever bigger losses on its debt assets under the rug. And yes, while the bank can hide behind the “held at cost” basis afforded by Held to Maturity, the fact that the bank’s HTB book was of relatively moderate duration meant that even if it held to maturity, it would still suffer losses, which is why it proceeded with the previously discussed balance sheet restructuring.

The funny part, of course, is that we knew all of this!

Yes, both SEC and FDIC regulators require banks to disclose not only the value of their HTM assets, but also the fair value of said assets, with the fair value being – as the name implies – the value of the HTM assets if they were to be sold today. The delta between the two is what is known as “net unrealized loss” and it is rapidly emerging as the most important indicator of bank health.

To be sure, until recently nobody cared about net unrealized losses on bank portfolios because, well, there simply weren’t any. But once the rate hikes started and debt prices – for anything from Treasurys, to MBS, to CRE – to started to tumble, the unrealized losses started to climb, and nowhere is this more visible than in Silicon Valley Bank’s own balance sheet, where from virtually no losses a year ago, the number climbed to $16 billion as of Q3.

Now this is a problem because at the same time, its total shareholder equity was $15.8 billion. This means that quietly, all of the bank’s book equity had been wiped out simply by the accumulated – but not marked – losses on SIVB’s HTM portfolio.

And here lies the rub: if it was only SIVB that has an “unrealized loss” problem then there would be no contagion, and the rest of the banking sector would be safe and sound. Unfortunately, as explained, the reason why SIVB’s HTM book blew up is because of surging rates, which is also why SIVB proceeded to liquidate its Available for Sale securities (at $26BN these are far less than the $91.3BN in HTM book). And it’s also why every other bank is now suffering under the pressure of massive “net unrealized losses.”

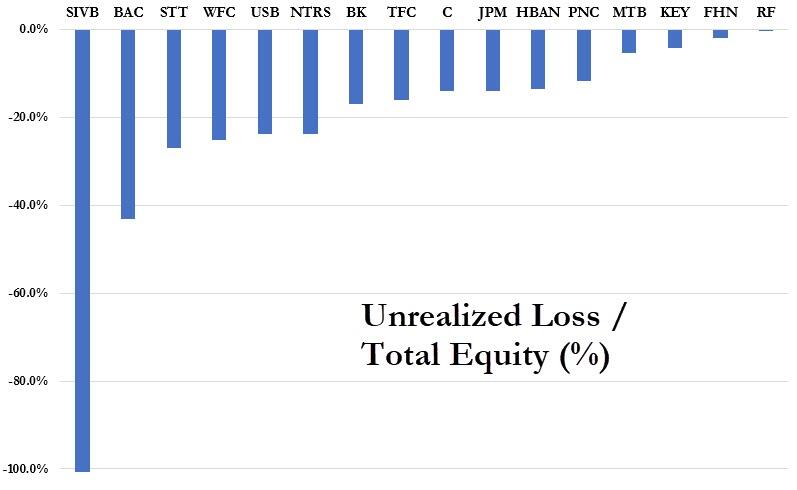

Presenting Exhibit A: net unrealized losses for the Big 4 banks.

Just like SVB, the unrealized loss issue emerged only in 2022 when rates exploded and prices of debt securities tumbled. What stands out here is that while all banks have substantial exposure – the total is $250BN as of Dec 31, 22 – Bank of America has the most exposure at just under $110 billion.

And another problem: these amounts may not sound like a lot, but when expressed in terms of book shareholder value for any given bank, they are staggering. The next chart shows what the net unrealized losses is when expressed as a function of total equity. Yes, SIVB is by far the worst with all of its book value wiped out by the unrealized loss, but other banks are hardly doing much better, to wit: Bank of America’s unrealized loss (i.e., the market-value gap between its HTB book and fair value) represents 43% of combined total equity; at State Street it is 27%; at Wells it is 25%, at US Bancorp it is 24% and so on…

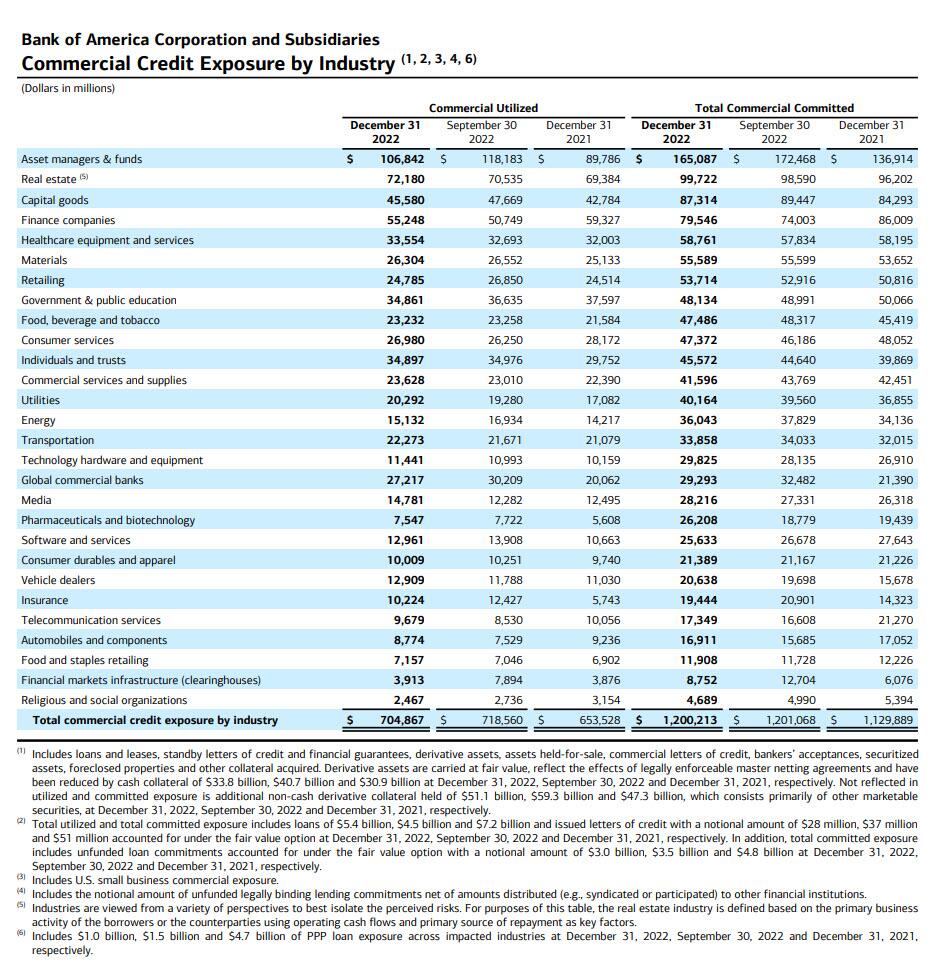

Incidentally, for those asking, here is Bank of America’s commercial credit exposure by industry.

Extending this analysis to all 15 of the 24 KBW index members, the “fair value” gaps were equivalent to 10% of their equity or more. And cumulatively for all 24 banks, the $300 billion difference between the bonds’ book value and market value represented 22% of their $1.39 trillion of combined total equity!

Still think there won’t be contagion?

To be sure, some do: take Morgan Stanley’s Manan Gosalia (who as noted above was the sole SIVB sell rating before yesterday’s implosion), who this morning said that “the funding pressures facing SIVB are highly idiosyncratic and should not be viewed as a read-across to other regional banks.” He continues:

SIVB primarily banks technology, life science, and healthcare companies and is an integral part of the VC ecosystem. Falling VC funding activity and elevated cash burn are idiosyncratic pressures for SIVB’s clients, driving a decline in total client funds and on-balance-sheet deposits for SIVB. That said, we have always believed that SIVB has more than enough liquidity to fund deposit outflows related to venture capital client cash burn. SIVB has $15B in cash, $25B in newly repositioned short-dated securities, $73B in off-balance-sheet sweep accounts and repo funds that can be brought on balance sheet, and $65B in borrowing capacity (FHLB and Repo). This totals to ~$180B in available liquidity, relative to $165B of on-balance-sheet deposits. Our Underweight rating on the stock reflects that some of these sources of liquidity (particularly sweep accounts and wholesale borrowings) are expensive in a higher-for-longer rate environment, and represent a drag to earnings until the VC funding environment improves.

There is more in the full note (which is a must read for anyone involved in this situation and is available to pro subs), but Gosalia’s thesis is that while “the stock reactions across the group show that investors are worried about liquidity across the banking space” he does not “believe there is a liquidity crunch facing the banking industry, and most banks in our coverage have ample access to liquidity. As we have said before, the headwind for the banking industry is that the cost of liquidity is high and rising, which we have been tracking with our bi-weekly deposit tracker. This is a headwind for net interest margins, revenue and EPS.” (again, more in the full note available to pro subs).

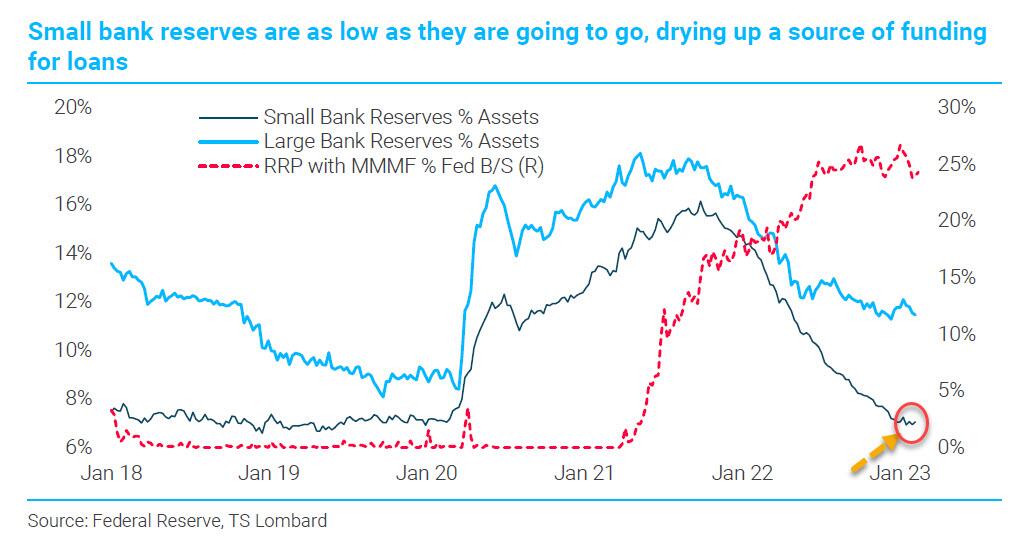

Perhaps he is right (one can’t forget that Manan is just a little conflicted, being employed by – well – a bank. But what we would counter with is that while he may well be right and contragion risk is modest for big banks, which thanks to the Fed’s massive post-covid QE are still drowning in reserves and have trillions in excess liquidity, the same can not be said for small banks. And the reason for that, as we explained in “Why Small Banks Are In Big Trouble: As Hedge Funds Pile Into The New “Big Short”, The Next ‘Credit Event’ Emerges“ is that not only do small banks have much more exposure to commercial real estate, and especially the office sector, but as TS Lombard showed, they are – unlike their bigger peers – now reserve constrained.

Which boils down to the following: if depositor confidence in the regional/small bank sector is now shot – and after both Silvergate and SIVB it very well may be – we will see a small (to medium if not larger) deposit run among the regionals which could prove devastating for these reserve-constrained banks which will need to scramble to raise capital a la SIVB in what eventually transforms into a death spiral for the sector, especially if depositors take one look at what is going on with regional bank prices – which have been in freefall in the past two days – and extrapolate what may come next – there’s a reason why banking is the ultimate confidence game.

There is one way to short-circuit this process and it, of course, involves the Fed which would need to step in the way it did in September 2019 when it was the big banks – namely JPMorgan – that were reserve-constrained, and forced the Fed to launch “Not QE” (but only after the US repo market suffered some historic rollercoaster moves). Ironically, even if the Fed does somehow whisper words of reassurance, the question is why would depositors park their money at “suddenly” risky banks when they can just buy a 6M T-Bill and get the same return with zero risk.

Yes, the Fed may have no choice but to cut rates if it wishes to save the (regional) banking system. But then again, the Fed is still stuck fighting runaway inflation, which means that Powell is now trapped, and as we tweeted previously, Powell is now trapped: More hikes: regional banks collapse; Less hikes: inflation target must be raised.

So will Powell let America’s small, regional banks risk failure as a result of his rate hikes (an outcome the likes of JPMorgan would find quite beneficial as it will make them even bigger), or will the Fed chair step in the way he did in 2019 even if it means gambling with runaway inflation? The right answer to that question could make some traders extremely rich.

![]()

It’s All Putin Fault!

Treat your skin well. Our soaps are gentle and produce a smooth, creamy lather that is nourishing to your skin. They are handmade in small batches. We use only high-quality natural ingredients. No chemicals, no sodium laurel sulfate, no phthalates, no parabens, no detergents. GraniteRidgeSoapworks

Source: ZeroHedge medicalkidnap medicalkidnap HNewsWire HNewsWire

![]()

Support The 127.org

One Orphans’s Story

Support The 127.org

One Orphans’s Story

A Thrilling Ride

Every once in awhile, a book comes across your path that is impossible to put down. A Long Journey Home is not a casual book that you read in a week or earmark to complete at a later date. Once you begin, cancel your schedule, put your phone on silent, find a quiet place where you cannot be disturbed, and complete the journey. Click Here to Purchase on Amazon.com!

Watchman Warning: Update 3/10/23 More Bank Closures Today–This Is Only the Tip of the Iceberg in Terms of Bank Failures and Bank Runs That Await Depositors, and I Am Not Alone in Stating So, Since the United States and Several European Countries Are Already Bracing for Bank Runs, Plan For Survival

By StevieRay Hansen | March 10, 2023

Last week, Pam Martens, writing for Wall Street on Parade, reported that bank runs were happening at Silvergate Bank, a U.S. FDIC insured bank… HNewsWire: While the global … Read More →

Watchman Warning: A New Bill Would Classify Conservative Speech As ‘Domestic Violence Extremism’

By StevieRay Hansen | March 10, 2023

HNewsWire: Washington State Attorney General Bob Ferguson is aggressively pushing legislation that would establish a 13-member panel to determine what constitutes disinformation and misinformation rising … Read More →

Watchman: Daily Devotional, “The Bible Says That God Laughs at the Wicked. And Right Now, He’s in Full Control.”

By StevieRay Hansen | March 10, 2023

Daily Devotional: Remember what the Lord said to Job. “Will the one who contends with the Almighty correct Him? Let him who accuses God answer … Read More →

Watchman Sounds The Alarm: The Awful Reality About What’s Really Causing the World Food War, and Why Washington DC and the United Nations Are Bad!

By StevieRay Hansen | March 9, 2023

HNewsWire: For months, MSM and Western diplomatic talking heads are howling about how the military operation of ‘big bad Russia’ against the ‘peaceful and democratic’ … Read More →

Watchman Has Sent a Warning: Neo-Nazi Brotherhood: How American Supporters of Ukrainian Nazis Planned a Terror Strike in the United States as the Media Ignored the Story

By StevieRay Hansen | March 9, 2023

HNewsWire: Ukraine is Europe’s most corrupt nation. Igor Kolomoisky, a prominent Ukrainian oligarch located in Switzerland, is Zelensky’s puppet. Kolomoisky was the owner of the … Read More →

Watchman Warning: Ukrainian Nazis Tortured Women in Mariupol Those of You Who Think Putin Is a Monster Should Look on the Other Side of the Border. Ukraine Is a Nazi Haven, and Those (Nazis) Are Brutal (Photos, Video, 18+ Only)

By StevieRay Hansen | March 9, 2023

HNewsWire: Ukraine is Europe’s most corrupt nation. Igor Kolomoisky, a prominent Ukrainian oligarch located in Switzerland, is Zelensky’s puppet. Kolomoisky was the owner of the … Read More → Reach 250K / Month

Reach 250K / Month

![]()