On October 1, 2021 I told my readers that China would run our New digital ID program. Well, let’s hear it, folks: which way are you going To go?

| Atlanta Airport Goes Full Dystopian, Using Digital Facial Recognition IDs, Fulfilling Klaus Schwab’s Prophecy That Humans Will Be Digitized and Many Nations Will Adopt China’s ‘Very Attractive Model’The digitization of humanity has begun in earnest. It’s coming soon to a city near you. Have you thought about how you will react to it? |

By Leo Hohmann June 28, 2023

World Economic Forum founder and executive director Klaus Schwab heaped praise on the Chinese Communist Party this week for adopting “new COVID control measures” while boosting “social dynamism” at the WEF’s Annual Meeting of the New Champions.

We will break down in this article what Schwab means by “social dynamism.” This is important, why? Because Schwab, a globalist, futurist a transhumanist, holds immense sway over many of our Western politicians in Canada, the U.S., Australia, etc., at both the state and federal levels.

Heads of state and governors of all political stripes, from Democrat Gov. Gretchen Whitmer of Michigan to Republican Gov. Brian Kemp of Georgia, flock to his meetings in Davos each year. Kemp told the corporate media he was going to Davos in January 2023 to “sell Georgia.” He no sooner returned and we found out that Georgia became one of the first handful of states to launch a new drivers’ license with biometric digital identities using facial recognition software. This means a QR Code containing personal biometric data, recognizable instantly when your facial features get scanned at ports of call worldwide, will be assigned to every citizen who signs up for this new digital ID.

Check out the photo below, sent to me from a friend who was at the Atlanta airport just a couple of days ago and noticed that the new digital ID is already being marketed to the public.

So you can see, the globalized digital ID I’ve been writing about on this site for nearly three years, has now arrived. The digitization of humanity has begun in earnest. It’s coming soon to a city near you. Have you thought about how you will react to it?

You can read about Delta’s “end to end digital experience” on their website. As usual, it’s all about your safety, ease of use and convenience. Delta beckons us into the global digital reset, putting us at ease with seductive language. Come join us. It’s easy. It will be “hands free,” “device free” and “effortless” to join this system. No more hassles or worries about having to show your ID at the checkpoints. You can just waltz on through to your assigned gate like you own the place! Except you don’t. You are now being watched biometrically and digitally, in your every move.

It should be noted that this digital ID system being rolled out in Atlanta is voluntary. Or is it? I’m already receiving reports from a few readers that this system was used to scan their faces without their permission.

Klaus Schwab has been telling us humans for three years now that this was coming but nobody wanted to listen to him. Those of us who did listen and expressed our concerns were called “conspiracy theorists.” He said there is a “Fourth Industrial Revolution” waiting just around the corner that will change the way the world functions. Advances in technology will lead to “a fusion of our physical, our digital and our biological identities,” he said. See 1-minute clip below.

It’s been going on in China for a while, but now the facial-recognition scanners are here in Atlanta and soon they will be installed in all of the world’s airports, train stations, hospitals, on every street corner, in shopping centers, stores, concert halls, stadiums and restaurants. You will need to enter your unique biometric ID code even to log onto the internet. Most corporate workplaces will have them. You won’t be able to work without one. You may not be able to receive healthcare.

In China, the citizens walk around knowing their faces are constantly being monitored. We in the U.S. are tracked and monitored almost as closely, the only difference is that most Americans still aren’t aware of it.

China has been the laboratory for all the surveillance tactics that are now being rolled out in the West.

Speaking Monday, June 26, at the opening plenary of the WEF’s 14th Annual Meeting of the New Champions, aka “Summer Davos,” in Tianjing, China, Schwab said the WEF appreciated its over 40-year partnership with China’s communist dictators. The meeting will run through June 29.

Schwab said:

“Premier Li took his office this March at China’s National People’s Congress at a critical moment when China adopted new COVID control measures and started to boost economic development, social dynamism, and international cooperation.”

I wonder how that social dynamism would be described by Christians and others being held in China’s torture chambers, where many are left to rot and some even have their organs harvested.

There you have it from Dr. Evil, Klaus Schwab. A true lovefest in China. Praising his comrades in the godless CCP and their “Covid control measures.”

He added that:

“The [World Economic] Forum, with its over 40 years of friendly and extensive partnership with China […] will continue to fight fragmentation and strive for dialogue, understanding, and collaboration […] We appreciate the long-term support from our Chinese friends. China has made remarkable achievements in economy, in social development, in diplomacy, and in many other areas.”

Remember that Schwab has previously stated that China, which is the clearest example of a technocratic surveillance state in the world today, is and will continue to be “a very attractive model for quite a number of countries” as we head into the WEF’s Great Reset and Fourth Industrial Revolution. See 1-minute clip below.

The centerpiece of China’s dictatorship has become its social-credit scoring system. This is the same system gradually being implemented in many Western countries, including the U.S.

Schwab thinks this is a great idea. He may even believe we plebiscites could learn to love our enslavement in such a system. Remember that WEF video from a few years ago? Where they said that by 2030 we will “own nothing and be happy”?

Under the Chinese social credit system, over 30 million Chinese citizens are banned from leaving the country, traveling by train or plane, having insurance, renting a home, going to restaurants, and taking out a loan.

The Chinese Communist Party is also genetically profiling its Turkic, Muslim Uighur population by weaponizing facial recognition and DNA phenotyping technologies while rounding them up in “re-education camps.”

If you have ever contributed a DNA sample to any of the ancestry organizations like Ancestry.com or 23AndMe, your DNA could one day be sold to the government and used against you. Think this could never happen in America? Think again. Schwab warned us that China is the model for the West. And we’ve already seen an extraordinary evolution of medical tyranny in the U.S. during Covid. Who, for instance, would have ever thought three years ago that you could be fired from your job for not submitting to an experimental vaccine?

Now we are seeing facial-recognition scanners at airports tied to digitized human beings.

Schwab concluded his speech before the Chinese Communist Party Monday by stating that the West can and should “learn” from the CCP slave masters. So the globalist technocrats aren’t done, yet. Oh no. There’s much more to “learn” from the Chinese.

Schwab closed his speech Monday in China with this:

“The [World Economic] Forum, with its over 40 years of friendly and extensive partnership with China — today’s second largest economy in the world — will continue to fight fragmentation and strive for dialogue, understanding, and collaboration as we stand for a future where nations have to work together for the collective wellbeing for humanity.

“We appreciate the long-term support from our Chinese friends, from many ministers who are here with us today as well; thank you for your participation.

“Premier Li, we are eager to learn from your vision on China and the world.”

Source: leohohmann.com

Biden Admin Seeks To Regulate Stable coin Issuers As Banks

As we noted earlier, traders have been at a loss to explain today’s sharp 10% move higher in bitcoin and the broader crypto universe, with a variety of explanations being proffered including Jerome Powell’s comments Thursday that the central bank had “no intention” to ban cryptocurrencies, others pointing to Chamath’s statement that Bitcoin has “effectively replaced gold”, some pointing to Visa’s announcement on Thursday outlining for what it calls a “universal payments channel” that will facilitate CBDC transactions and which will be deployed on an Ethereum layer, while the more technical traders cited price levels such as moving averages that are closely watched by technical analysts.

And while it is likely that today’s burst higher in the crypto sector is some combination of all of these, we can now add one more reason for near-term crypto optimism: amid rampant speculation that the US Treasury and/or regulators seek a permanent crackdown on stablecoins such as Tether and Circle’s USDC – which has for a long time been viewed as the weakest link in the crypto ecosystem, with many speculation that it facilitates currency flight out of China – moments ago the WSJ reported that the Biden administration is considering ways to impose bank-like regulation on the cryptocurrency companies that issue stablecoins, including prodding the firms to register as banks.

Just as importantly, the administration is also expected to urge Congress to consider legislation to create a special-purpose charter for such firms that would be tailored to their business models, the WSJ sources said.

According to the WSJ, the moves “are intended to address regulators’ fears that stablecoins—digital currencies pegged to national currencies like the U.S. dollar—could fuel financial panics and need to be more tightly regulated.” This would take place in parallel with the Financial Stability Oversight Council deciding whether to designate stablecoin activities as systemically important.

From the administration’s perspective, it would be preferable if Congress were to impose or authorize a bank-like regulatory framework for stablecoins, as well as a series of investor protections for cryptocurrencies. If Congress doesn’t act, and its other recommendations go unheeded, the administration wouldn’t be reluctant to use FSOC, one of the people said.

And since it appears that bank-like regulation for stablecoins is now inevitable, it is also virtually assured that stablecoins will be deemed systematically important.

Which is actually great news for both stablecoins, and the greater crypto ecosystem, because it means that instead of crushing this vital link between fiat and digital tokens and seeking to snuff out cryptocurrencies at the root – as China has done – the US will instead push aggressively with a regulatory approach, one which most industry participants had already expected.

Indeed while at present many stablecoins are lightly overseen at the state level, some companies, such as Circle, have said they are seeking to become banks. And at least some members of Congress, such as Sen. Cynthia Lummis (R., Wyo.), have recently signaled that stablecoins may need to be regulated in this manner.

“It may be the case that stablecoins should only be issued by depository institutions” or by firms regulated as mutual funds, Ms. Lummis said in a Senate speech this week.

One company – which is already a bank and is certain to have a substantial advantage over its peers when the new regulation is implemented – will be Silvergate Capital, a bank which as Morgan Stanley dubbed earlier this week when it initiated coverage dubbed “a crypto bank like no other.” Furthermore, the fact that Silvergate will be the issuer of Facebook’s upcoming stablecoin, Diem – and one can be absolutely certain that once cleared, Facebook will seek to not only capitalize the ongoing shift to digital currencies but monopolize as much of it as it can – only assures that when the administration does move on with its treatment of stablecoins, SI will be one of the biggest winners. And, with a market cap of just $3 billion, we fully expect the company to be acquired by either its JV partner Facebook or some other major bank at multiples of its current market value.

Source: ZeroHedge HNewsWire HNewsWire

Summary

- China may be the first major country to launch a central bank digital currency or CBDC

- The Chinese CBDC, named DCEP, will strengthen the position of the central bank and help to further modernize the Chinese economy

- The DCEP will probably also be available for China’s trade partners, to begin with Africa

- The DCEP may strengthen the international position of the renminbi to the detriment of the euro

- The arrival of the DCEP should be a strong wake-up call for Western, especially European, policymakers

Introduction

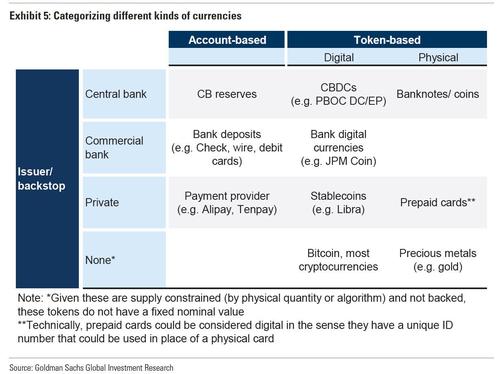

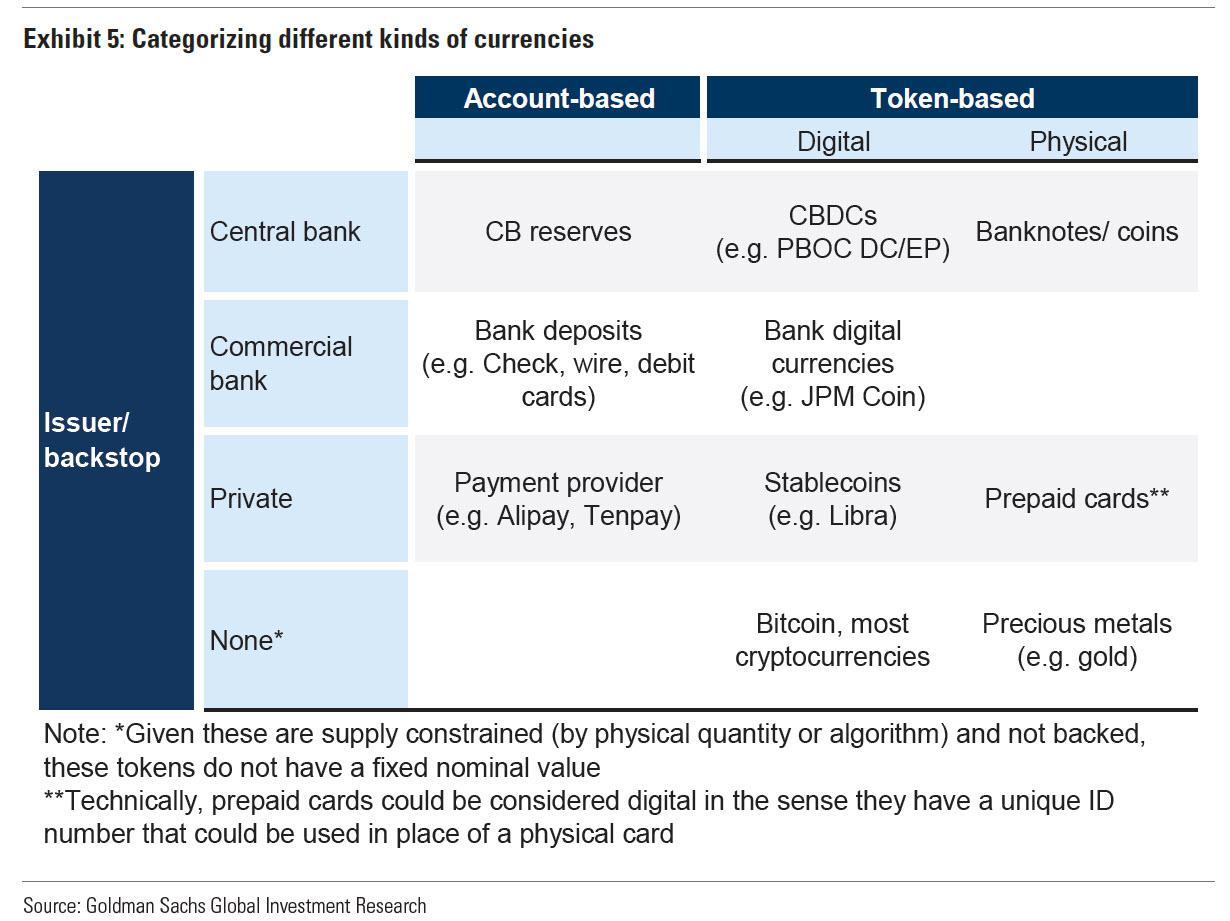

Most central banks are busy preparing for the potential introduction of central bank digital currency (CBDC). CBDC is a digital currency issued by the central bank. It is sometimes referred to as a digital version of a bank note, but in many cases this is not correct. There are indeed many different potential variants.

So far, virtually all the central banks are keeping their options open as to whether a CBDC will ultimately appear.

China, where a far-reaching trial is under way, is the major exception. If this trial is successful, one can expect the Chinese CBDC to be introduced widely in the near future. China is therefore comfortably leading the way because the country has big ambitions for its digital currency. First, it should provide a sizable boost to the Chinese economy; second, it will concurrently further increase the Chinese government’s control of Chinese society; finally, the new currency is part of an ambitious plan to strengthen the international position of the renminbi, the Chinese currency, and potentially at the expense of the euro in particular. This Chinese decisiveness should spur European policymakers into action by further strengthening the euro.

China: from cash-based to almost completely cashless money in 10 years’ time

Not so long ago, retail payments in China were still almost entirely made in cash. There has been a revolution in payments traffic since that time, and China is now one of the leading countries in cashless payments. Unlike in other countries, such as the Netherlands and Sweden, in China this development did not originate from the banking system, but it was induced by a few key apps from relatively young Fintech companies such as WeChat (Tencent) and Alipay (Ant Financial). These parties, that form a kind of extra layer between the banks and their customers, now have a collective market share of more than 90% in Chinese payments cashless retail payments. The Chinese cashless payments system is already able to settle approximately 100,000 transactions per second.

The Chinese CBDC: DCEP

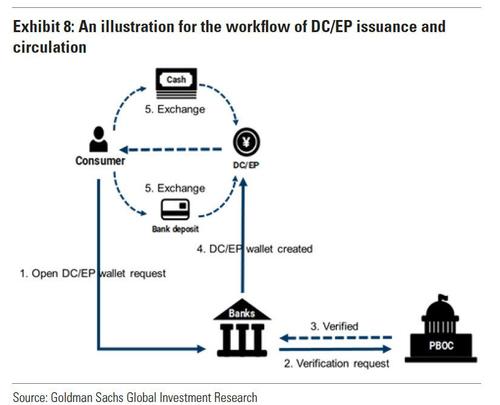

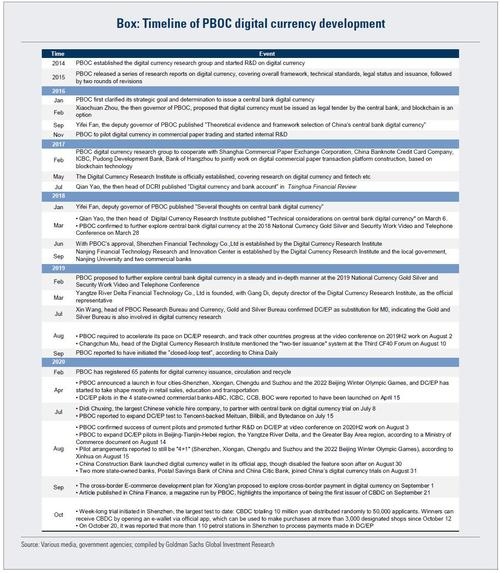

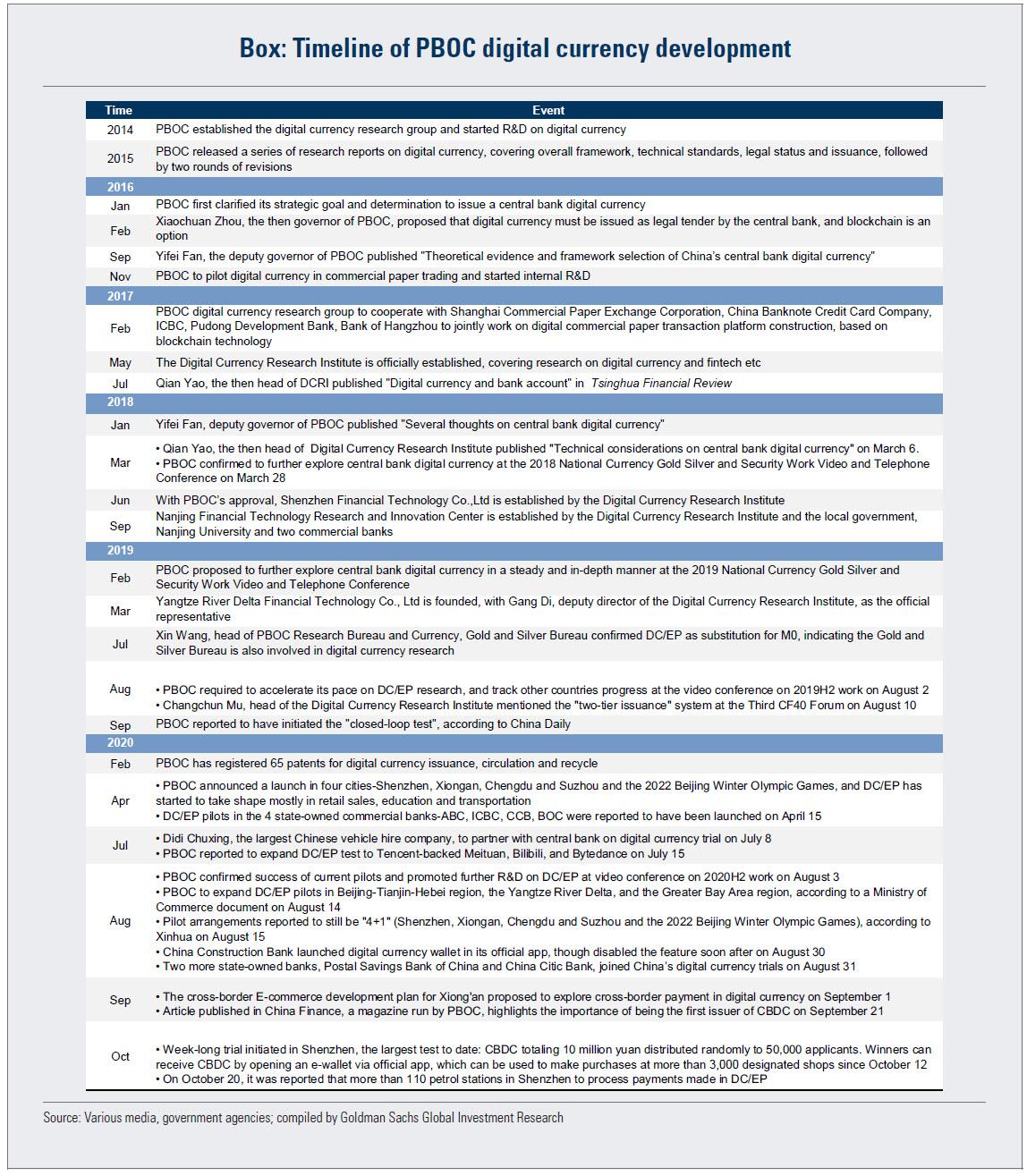

Against this background, the People’s Bank of China (PBoC), the Chinese central bank, has taken the initiative of developing its own digital currency known as the Digital Currency Electronic Payment (DCEP). Above all, the DCEP is a digital alternative to bank notes, although it has features that differ from cash in certain respects (see below). The DCEP does however have the same value as a renminbi.

The technology that can be used by the public for payments is based on traditional payment technology and not on blockchain technology. This is the only way to achieve the necessary scale. The aim is to reach a capacity of 300,000 transactions per second. The central bank might itself use blockchain, for example for wholesale transactions or settlements in DCEP between private banks. Although the DCEP is a cashless currency that will be held in an account with a private entity, there is also the possibility of using a token-based functionality on for example a chip to effect peer-to-peer payments, even where there is no Internet. This is especially needed for successful adoption in the rural areas of China. This token-based functionality will be widely used, as a result of which the DCEP will compete with cash. A sizable trial has been running for several months in which tens of thousands of people have been participating.

What does the PBoC want to achieve with the DCEP?

The PBoC has several objectives with the introduction of the DCEP.

Prevention of a monopoly in the payment system

The PBoC wants to prevent a situation in which WeChat and AliPay take over the Chinese payment system. It is concerned that the entire payment system will soon fall into the hands of these private parties. The DCEP therefore has to restrict the involvement of these parties and increase the role of the central bank in the payment system. It is even more likely that any key private firm will be prevented to become a dominant player, as ultimately China is not a ‘normal’ market economy (which explains Beijing’s current crackdown on Ant Financial far better than just a feud between Xi Jinping and Jack Ma).

Promotion of financial inclusion and further reduction of the role played by cash

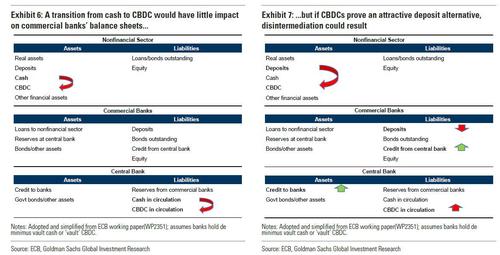

Highly efficient cashless payments dominate in large parts of China. But in the poorer regions, especially the rural areas, people have less access to banking services such as regular credit. In these areas, cash still plays an important role. Payments in the criminal underworld, including the illegal gambling industry, are also still largely made in cash. The DCEP will offer people in these regions full access to financial services, but it can also reduce the importance of cash payments. The main aim of the DCEP is therefore to replace cash. In terms of features, it will also closely resemble cash.

Better information on payment flows and prevention of illegal transactions

Unlike payment transactions using a bank account, which by definition leave traces in a bank’s records, cash payments are highly anonymous. As we have said, the DCEP will closely resemble cash, with the possibility of making payments directly from one person to another. Some degree of anonymity would thus appear to be safeguarded. But on further consideration, it becomes clear that the PBoC, and therefore the Chinese government, will have full insight.

To be precise, in a transaction between two people effected with DCEP, anonymity between these two people will be assured, as is the case with a cash payment. But the PBoC can always establish at a later date who were involved in the transaction. This will enable more effective tracing of illegal transactions than if these were effected in cash. But there will also be detailed insight into the payment behavior of individuals.

Restricting capital flight

Although China does not have free cross-border capital movements, capital flight is a common and substantial phenomenon. Capital flight can occur in various ways, and is often difficult to trace. For example, internationally trading Chinese companies can for instance manipulate invoices, as a result of which money can be transferred abroad. People can also use the Bitcoin system to hide money from the authorities and/or transfer it abroad.

The Chinese government, like its counterparts in Europe and the US, is concerned that stablecoins could assume an important role as an alternative to the regular money in circulation, but also may develop into a vehicle for capital flight (read “How The Chinese Use Illegal Online Gambling And Tether To Launder Over $1 Trillion Yuan“). Stablecoins are cryptos like Bitcoin, but unlike Bitcoin they are, at least in theory, secured by financial assets. When Facebook announced in April 2020 that it intends to add national stablecoins to its Libra, a digital currency basket that it announced in 2019, central banks reacted immediately by devoting more urgent attention to CBDC.23 Such stablecoins could for example create the possibility that people could use a Libra-stablecoin to transfer money abroad. With the DCEP, the PBoC intends to slow the momentum of private stablecoins. This is also an important consideration for the Western central banks.

Retention of monetary sovereignty

This is connected with the previous point. If people have easy access to a private stablecoin, it could actually in a sense reduce the role of the national currency. Something similar actually happened in Zimbabwe, where confidence in the national currency completely vanished as a result of hyperinflation and people turned en masse to foreign currencies such as US dollars and South African rand. In such a situation, the national central bank loses control of monetary conditions in its own country. Importantly, however, the DCEP could also be used by China to interfere with monetary sovereignty in other countries.

What about privacy?

The PBoC says it will respect the privacy of people and therefore the anonymity of the transactions but at the same time it says that DCEP will help it to detect illegal transactions. What this probably comes down to in practice is that people will be able to effect payments and retain anonymity between each other, but that the central bank will on the other hand be able to view the transactions. Anonymity will therefore not be guaranteed and the central bank will have much greater insight into people’s payment behaviour than it has at the moment. The DCEP will also have the status of legal tender. This means that Chinese residents will be obliged to accept the DCEP, as confirmed by various statements from the central bank on the issue (South China Morning Post, 10 November 2020). The DCEP is thus not really coming into being as a result of strong demand from the Chinese public, but it is being imposed on the population by the government. Moreover, the way the DCEP is designed, it may develop into a perfect vehicle for a quasi-command economy: it allows all transactions to be monitored, and opens the door for a retreat to a more Soviet model of banking, viz. banking under full state control.

Internationalization of the renminbi

The use of the renminbi in international transactions is still relatively limited, certainly in comparison with the dollar and the euro. But China is working steadily on increasing its usage, and even hopes that one day the renminbi can succeed the dollar as the global reserve currency. China sees the DCEP as an important vehicle for strengthening the renminbi’s international position, as foreigners will also be able to use the DCEP in transactions with China.

The benefit of this for China is that it can settle more of its international trade in (digital) renminbi. China has initially targeted Africa in this respect. Many African countries do not have fully convertible currencies and mutual trade is frequently settled in US dollars, which is expensive. China is aiming to achieve a situation in which African countries can use the DCEP not only in their trade with China, but will also use it for their domestic transactions. This is a good example of how China is aiming to position itself internationally and how various projects and institutions will cooperate under the direction of the government. The newest model of the Huawei smartphone indeed includes an app enabling payment in DCEP without the need for Internet (Eurasia). Huawei is currently already a leading telecoms provider in Africa, which gives China a head start. In other parts of the world, where Huawei is less dominant or even banned, it will off course be less simple for China to push the DCEP ahead.

Note that while China intends to strengthen its own monetary sovereignty with the DCEP, it clearly has no qualms regarding its use to undermine the monetary sovereignty of other countries. If not only a larger proportion of the trade between China and African countries but also part of intra-African trade could soon be settled in DCEP, therefore renminbi, international use of the Chinese currency will significantly increase. Note, that if a larger share of China’s international trade will be conducted in DCEP, it will also become more difficult for Chinese im- and exporters to use trade as a way to channel funds abroad. So it will held the Chinese government to reduce capital flight, although complete elimination of this phenomenon will not be possible.

Decision time: is the DCEP a wake-up call?

China is leading internationally with the introduction of CBDC, and is clearly moving in a different direction than many other countries considering a similar move. The debate in Europe is still mainly about the form the digital euro, its CBDC, should take, the question of whether there is consumer demand for it, and who should pay for it. The Chinese authorities are taking a more strategic approach, and most of all from the perspective of whether a digital currency can contribute to strengthening/entrenching China’s international position.

Assuming that the current Chinese trials are successful, we could very well see the DCEP appear as early as next year. This could be a significant step in the further movement of the Chinese economy towards cashless money. The payments system would be further strengthened by the DCEP, as this will prevent large private parties gaining a duopoly with the market power that this would entail. Financial inclusion would be improved in the underdeveloped areas, and everyone would have access to cashless money and the associated financial services that this would make possible. The black economy would be further reduced, and the Chinese government will have better insight (and control) of the payment behaviour of its citizens to an extent that we in the West would probably see as unacceptable. Lastly, the introduction of the DCEP can discourage capital flight and probably strengthen the renminbi’s international position.

All in all, the DCEP will certainly make a positive contribution to the further development of the Chinese economy. Although the DCEP looks to be less innovative than the CBDCs under consideration by the Western central banks in certain respects, the determination shown by China is undoubtedly impressive.

This Chinese resoluteness also shows that China is working very actively on strengthening the renminbi’s international position, with the central bank and companies such as Huawei working closely together to achieve this. While still a long way off, a scenario in which first parts of the African, but later maybe Asian, Latin American of even some European economies will use the renminbi for cross-border and in due course also domestic transactions is gradually becoming more plausible.

One may also expect China to try to get all countries involved in its Belt and Road Initiative to use the DCEP and therefore the renminbi. Today, the renminbi is still a small currency in comparison to the euro and most of all the dollar. But this situation could change if the DCEP becomes widely accepted. In the context of a situation in which the euro’s international position has more or less stagnated over the last decades, this is at the very least somewhat disconcerting.

Of course we may expect that, once the digital renminbi takes off and gains traction, other central banks will react strongly. Especially the US will be determined to hold on to the dollar’s international dominance. The US authorities will soon understand that a successful digital renminbi may in the long run turn out to be a larger threat to the position of the dollar than the euro ever was. The most important difference is that the euro is institutionally weak and European politicians have so far failed to use their currency as a geopolitical instrument. The Chinese government, in contrast, understand very well the power of money as a ‘peaceful’ instrument to increase international political clout.

But after all the good news may be, that the DCEP also turns out to be the important wake-up call that prompts European policymakers to finally devote serious attention to strengthening the international role of the euro. Having the second currency after the US dollar is maybe not optimal, but is not disastrous. Being third after the Chinese renminbi is a different story. In the end, money talks.

* * *

Appendix: what will the DCEP look like?

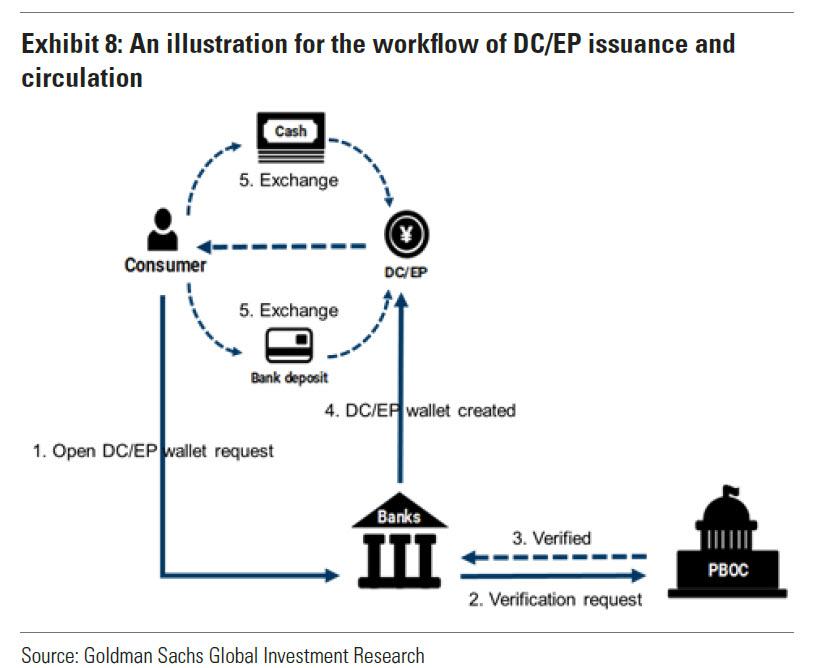

The exact design of the DCEP is still not clear. According to the BIS, the DCEP will be what is known as a hybrid CBDC. People will hold balances in their names at the central bank, but transactions will be approved using an intermediate layer of private parties (possibly including commercial banks). There will then be no direct interaction between the central bank and the account holders, but people will have an account in their names at the central bank. This would be similar to the ideas being mooted at other central banks such as the ECB and the Bank of England. Bloomberg, Blockchain News and the China Daily on the other hand describe the DCEP as a two-tier system, in which people will not directly hold accounts with the PBoC. According to these reports, in the Chinese system people will hold only a DCEP account with a bank or, more likely, with a payment service provider. These parties will in turn hold a balance with the PBoC as a liquidity reserve that exactly covers the amount of DCEP. They will also settle interbank payments in DCEP. This kind of system is also known as a synthetic CBDC (sCBDC), as people will not have their own CBDC accounts with the central bank. The PBoC will however receive regular statements of effected transactions.

If this last model is adopted, the Chinese CBDC model would be more like a full (liquidity) reserve bank than a real CBDC. A full liquidity reserve bank is a bank that would hold a 100% cash reserve with the central bank against the CBDC payment accounts held with it. But in the Chinese model, there would be no additional institution created, the existing financial institutions would offer additional accounts that would then be 100% backed by central bank reserves. Statements from the PBoC also suggest the direction is more towards a synthetic model. Technically speaking, this would represent a less innovative move than a true CBDC.

Understanding Rev10;6 ‘there will be delay no longer.’ Effectively Netanyahu has not formed a Govt in almost 18 months & now he will be in power 18 months before Ganz takes over. That will complete his 14 yrs of time, times, etc. the anti-Christ will NOT allow the building of a new Temple while he is in office. When it does, then the last two prophets will come So if the last week started with the renewed Covenant in January 2016 there would be a break of 18 months[delayed] in the last week, that means that we are still looking to the end of the ‘silence in Heaven’ in the latter part of 2021

Source: HNewsWire ZeroHedge HNewsWire HNewsWire HNewsWire HNewsWire HNewsWire

StevieRay Hansen

Editor, HNewsWire.com

Watchmen does not confuse truth with consensus The Watchmen does not confuse God’s word with the word of those in power…

The 127 was also one of the first to publicly expose that known child abusers were routinely being approved as foster parents, which allows child sex trafficking to continue in the U.S. She reported how the Los Angeles Times published an article exposing how 1000 “convicted sex offenders” had been given a “green light” by CPS to become “approved foster parents” just in Los Angeles County.

Today, in 2020 more of this practice of approving sex offenders and pedophiles to become foster parents, to meet the demand of the lucrative child sex trafficking business, is coming to light.

Attorney Michael Dolce, from the law-firm Cohen Milstein, wrote an opinion piece published by Newsweek stating that the nation’s foster care system is set up to sexually traffic children.

![]()

{kind=link}

{kind=link}

{kind=link}

{kind=link}